Income-Tested Care Fee Explained: Who Pays and How Much?

When planning for aged care at home, understanding the Costs Involved in HCP is just as important as choosing the right support. While the government subsidises most of the cost through Home Care Packages (HCPs), you may be asked to contribute based on your financial situation.

One of the most commonly misunderstood contributions is the Income-Tested Care Fee (ITF).

In this blog, we’ll clearly explain:

- What is the Income-Tested Care Fee ?

- Who may need to pay for it? (and who won’t)

- How is it calculated?

1. What Is the Income-Tested Care Fee?

The Income‑Tested Care Fee is a contribution some individuals pay towards their HCP services, based solely on income, not assets. Services Australia uses the SA456 form to assess it, and if applicable, the fee is added directly to your package budget, funding services like personal care, transport, nursing, or domestic support.This isn’t an extra charge or a penalty, it’s a means-tested contribution that helps make the aged care system fair and sustainable for everyone.

2. Why does the Income-Tested Care Fee exist?

The Australian Government helps fund most of the cost of Home Care Packages, ensuring older Australians can access the care they need to live independently. However, to keep the system fair and sustainable, people with higher incomes may be asked to contribute through the Income-Tested Care Fee.

This approach ensures that:

· Those who can afford to contribute do so, while

· People on lower incomes pay less or nothing at all

To protect your financial wellbeing, there are strict limits on how much you can be asked to pay:

· Annually: You won’t pay more than a set amount each year.

· Lifetime: Once you reach the lifetime contribution cap, you will never have to pay the Income-Tested Care Fee again, even if you later move into residential aged care.

As of March 2025, the lifetime cap is $82,347.13.

3. How ITF Works Within Your Home Care Package?

The Income-Tested Care Fee (ITF) plays an important role in how Home Care Packages (HCPs) are funded. It doesn’t reduce the value of your package. Instead, it helps share the cost of care between you and the government based on your ability to contribute.

Here’s how it works:

· Your Home Care Package Has a Fixed Value:

Each HCP level (from Level 1 to Level 4) comes with a set annual budget. For example, a Level 3 package is worth around $34,550 per year.

· Your Fee Replaces Part of the Government Subsidy:

If Services Australia assesses that you need to pay an ITF, your contribution simply reduces the government’s share, not the total package amount.

Example:

- Package Value: $30,500

- Your ITF: $4,000

- Government Pays: $26,500

- You still receive $30,500 worth of care services

The ITF isn’t lost or paid to the government. It goes directly to your approved provider and is used entirely for your care - such as personal care, cleaning, allied health, or nursing support.

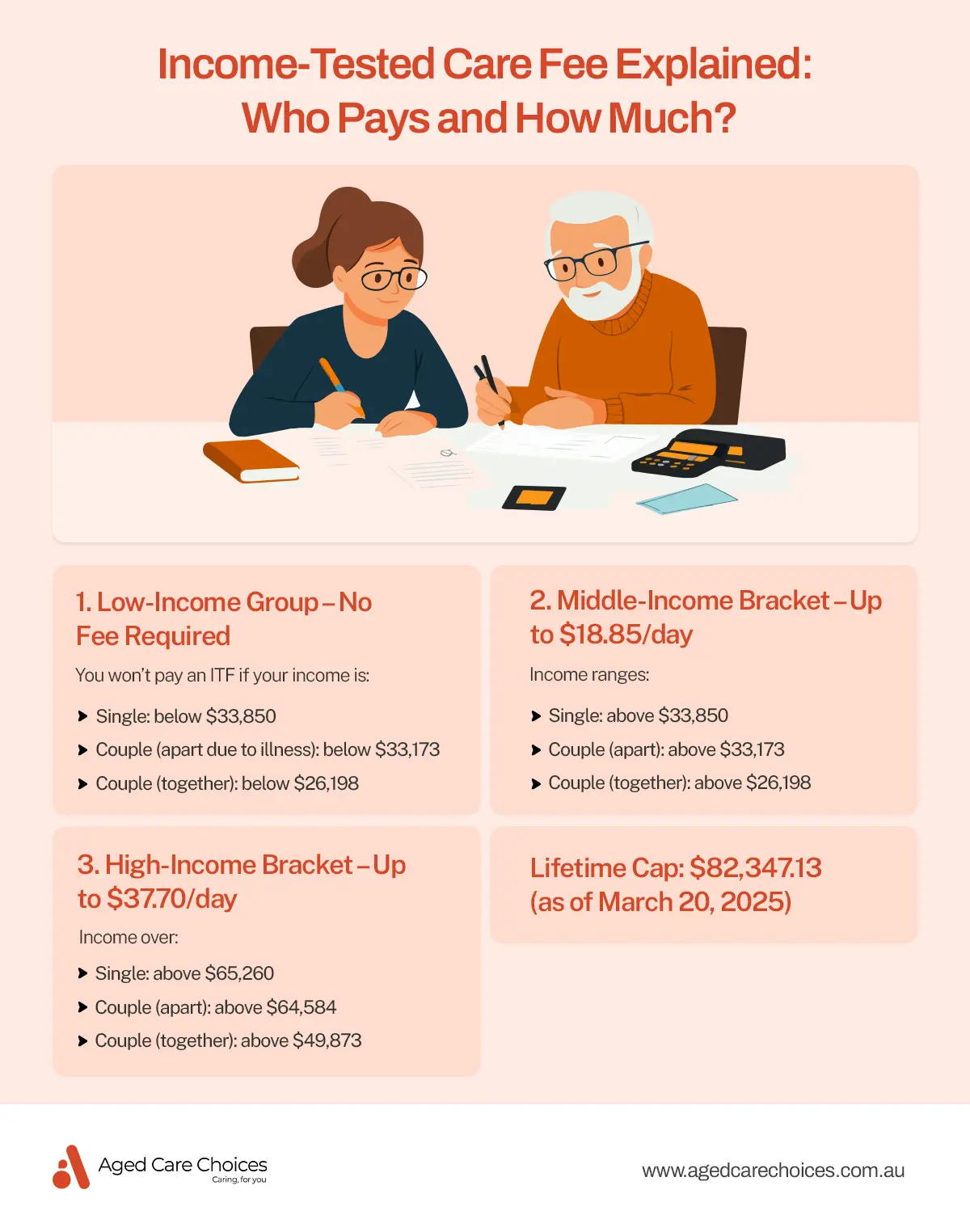

4. Who Pays and How Much?

The Income-tested fees are not charged to everyone. Your liability depends on your assessed income:

Lifetime Cap

· Maximum Payable Over a Lifetime: $82,347.13

· Once this cap is reached, you won’t pay any more ITF, even if you later enter residential aged care.

5. How Is ITF Calculated?

- The SA456 form captures your taxable income and Medicare levy.

- Exclusions include pension supplements and rent assistance.

- Services Australia reviews your information and shares the finalised amount with you and your provider.

- Your contribution is deducted for the government subsidy.

Reviews occur automatically in March and September and earlier if your income changes significantly.

6. What If Your Income Changes?

Your income is automatically reviewed twice a year in line with government indexation. This ensures that any changes to your financial situation are reflected in your Income-Tested Care Fee (ITF). However, if you experience a significant shift in income and can’t wait for the scheduled review, you can request an earlier reassessment by submitting a new Income-Tested Fee assessment form. Updates ensure fair contributions, and may reduce or eliminate your fee if your income falls.

For more information, visit the Changes to Aged Care Fees page on My Aged Care.

7. Myths about ITF

- ITF reduces my care value. False, it replaces subsidy but doesn’t reduce your HCP budget.

- The government keeps ITF. False, the fee goes to your provider for agreed care.

- ITF is fixed once set. False, it’s updated with your income or indexation changes.

Conclusion

Understanding the ITF is key to planning your care journey. Remember:

- Some people won’t pay it at all.

- It’s income-based only.

- Your HCP’s total value remains intact.

- Contributions are capped annually and over your lifetime.

How Aged Care Choices Can Help?

Aged Care Choices guides you through every step - submitting the SA456, interpreting your fee advice, calculating your potential costs, and ensuring your care plan maximises your funding. We support you in managing your ITF obligations so you can focus on receiving high-quality care at home.

FAQs

- Do full Age Pensioners pay ITF?

No. If your income falls in the low bracket, you won’t pay. - Does ITF reduce my package value?

No. Your full package amount remains available; ITF simply replaces part of the government subsidy. - Can ITF change mid-year?

Yes. If your income significantly changes, you can request a reassessment. Otherwise, updates occur in March and September. - Is there a payment cap?

Yes. A daily cap, annual cap, and a lifetime cap of $82,347.13 as of July 2025. - How does ACC support?

We help with assessments, calculating fees, wellness planning, and selecting a provider who uses your full package budget effectively.

Related Blog Posts

You’re Not Alone in This Journey!

Now find the right aged care provider for you. Fill out a quick form and get matched with trusted services in your area.